Perma-bears can meet their demise in one of two ways: slow starvation (sticking to a bearish bias over decades and slowly, but surely getting left behind), and self-immolation (holding dearly to bearish positioning during a major run-up and finally flipping bullish at precisely the wrong time).

*****

I’ve been trying to write a follow-up post to the one I wrote in January 2022 for six months now. It’s been a struggle. Seth Klarman recently noted “this is one of the weirdest environments in the 40 years I’ve been in the investment business.” I agree, even if I haven’t been around quite as long.

Eighteen months ago, the possible routes ahead seemed clear: speculative growth may soon be gone and dead “forever” (until the next bubble) or value investors would be forced into retirement. As the tide went out in 2022, speculative growth types got obliterated. Despite this revealing episode, most not only survived, but have been given second chances[1]. Even more amazingly – to me at least – they and their forgiving backers have been redeemed in spades year to date.

While I acknowledge (and try hard to fight) my own cranky tendencies, I can’t help but wonder if celebrations might be premature. A few miscellaneous things have popped up in recent weeks that have my antenna up:

Short-sellers are on life support. Via Goldman Sachs (data as of July 19): “[The GS] Most Short basket 2-month relative returns to SPX is 23% today, which is the 4th highest return spread since 1-Jan-2010 (looking at 2m returns daily), and ranks in the 99th percentile” (emphasis mine).

Longs are full risk-on. Via Man Group: “the drawdown in the MSCI World [Minimum Volatility] Index (relative to the standard index) has reached an extreme level that is only comparable to the DotCom tech bubble and the post-Covid market risk rally.”

The CRE crisis is very real, based on recent discussions with various industry contacts. Perhaps CRE issues are and will remain well-contained, but the contrast vs. the exuberant “we stuck the (soft) landing” high-fives is very peculiar.

The yield curve remains deeply inverted and its signal value is widely mocked at the moment. My view on the yield curve is that much like inflation, its impacts are serious and hard to predict.

What does it all mean? I think it paints a picture of investors eager to move on (and up). I don’t blame them. A clean break from the macro weirdness of the last 18 months would be nice. Historically though, I don’t think that’s how hiking cycles have played out. Like the 2020-2021 SPAC bubble, perhaps the logical outcome will take longer to unfold than expected.

For at least two notorious perma-bears that I track, it’s already been too much[2].

- - George - -

*****

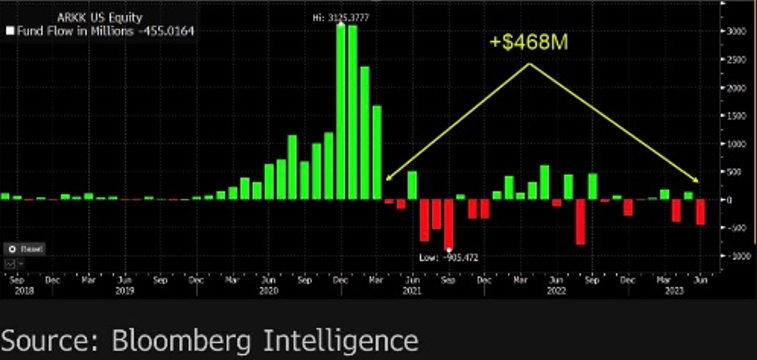

[1] See Ark flagship fund flows below.

[2] One hot off the press, the other I’ll keep to myself - sorry. Addendum: to be fair to Morgan Stanley’s Mike Wilson: (a) recent history aside, I’m not sure he could fairly be described as a “perma-bear.” But, for now he is certainly the face of the bear crowd. (b) he hasn’t fully “capitulated” yet - just rightly acknowledged mistakes to date. For the record, this post wasn’t originally intended to be about him!

Fund flows for Ark Investment’s flagship fund (ARKK). I acknowledge the chart crime-y summary label, but am astonished net flows haven’t been far worse.