I have long been fascinated by Russia. I studied the language and history in high school and college and have visited the country many times. As recently as 2020, I told my wife I hoped we could visit Russia with our children someday soon. I really want(ed) to get back to St. Petersburg.

None of this makes me anything close to an expert on China. But I believe it has provided some essential perspective on the speed and violence with which things can change in emerging markets. I went from being earnestly (naively?) hopeful that maybe, possibly Russia could turn things around to sickening disappointment in a very short period.

I have written (okay, Tweeted) a lot about China over the past year. I think about it constantly because I think its path impacts much of the world, as well as all global and many domestic businesses. Despite macro and geopolitical headwinds, investors continue trying to bottom-tick Chinese stocks. I am sympathetic to the logic: sentiment is truly horrendous, valuations are cheap, and aggressive stimulus measures have historically been the norm (and is there anything more certain in life than stocks booming on aggressive stimulus?). Ironically, I think these knife-catchers gain intellectual comfort from the Taiwan debate. Mainstream talk of a doomsday scenario – which everyone knows is very remote – is just another sign that sentiment must be bottomed out. Betting against a Taiwan invasion feels bold, but completely rational.

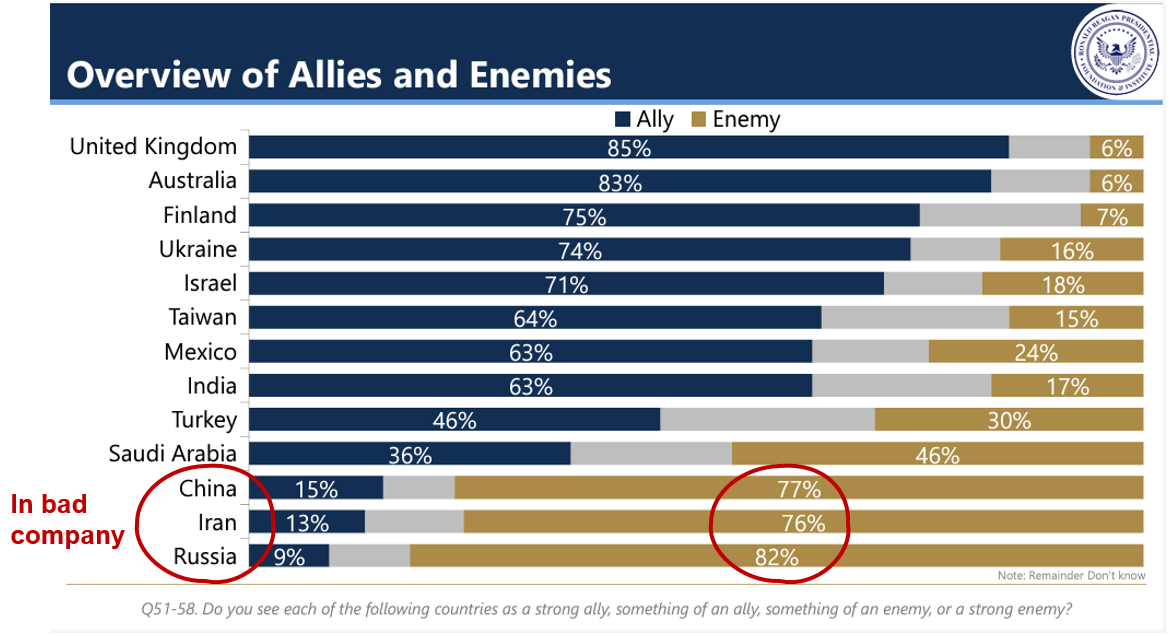

The problem though, isn’t the specific Taiwan risk but what’s driving it. This partly explains the inconsistency of Taiwan Semiconductor (and Apple) shares sitting a stone’s throw from all-time highs, while major Chinese equity indexes sit at multi-decade lows. If growth prospects were solid, would investors be eager to gain exposure to Russian or – pause for laughter – Iranian stocks today? Why not? China has not-so-slowly moved in this direction – cozying up with…Russia, Iran and other sworn enemies of the United States in words and actions. Military harassment of U.S. allies happens regularly. This isn’t some Zerohedge conspiracy theory. On a bipartisan basis, Americans view China as a clear “enemy” of the United States that represents the country’s “greatest nation-state threat” (see charts below). Political and military leaders agree.

“You want it to be one way. But it’s the other way.” – The Wire

Wall Street is the laggard – still mostly viewing China as investable (if out of favor) and analyzing it through the traditional lens of valuation, sentiment, and macroeconomics. But something is missing – and it’s as foundational as it is blindingly obvious. China has rapidly become un-investable for moral (not really the correct word, but you know what I mean) reasons. Quite simply: we don’t invest in stocks of countries actively trying to harm us. It feels uncomfortably judgmental and unscientific to seriously consider this in an investment analysis. But, work through the logic and you’ll see it quickly ties back to fundamentals: over time, companies operating in such countries will almost certainly face unpredictable and serious blowback.

Given the events of the past 5+ years, this isn’t hard to imagine. While Russia represents a worst-case scenario, China itself has already faced plenty of (growing) consequences. In my view, investors would be well-served to quickly become far more judgmental when it comes to investing in companies based in countries that are undemocratic adversaries of the United States.

Finally, what might it take for Chinese equities to reach a sustainable (as opposed to tradable) bottom? I think the answer is obvious: a sustained reversion of the polling data shown in the charts below (note: I selected this particular poll for convenience, but I believe it is fairly consistent with many others). It’s really hard to know what the catalyst could be, but I think investors should be clear that this is the bet they’re making today. I hope it’s a good bet.

Source: Ronald Reagan Presidential Foundation & Institute - 2023 National Defense Survey

Note: red annotations = mine

Source: Ronald Reagan Presidential Foundation & Institute - 2023 National Defense Survey

Note: red annotations = mine

Source: Ronald Reagan Presidential Foundation & Institute - 2023 National Defense Survey

Note: red annotations = mine